A Detailed Overview of Secured Credit Card Singapore Options for Enhanced Credit History Control

A Detailed Overview of Secured Credit Card Singapore Options for Enhanced Credit History Control

Blog Article

Deciphering the Refine: Just How Can Discharged Bankrupts Obtain Credit History Cards?

The procedure of restoring debt post-bankruptcy presents one-of-a-kind obstacles, commonly leaving many wondering about the feasibility of obtaining credit history cards once again. Exactly how precisely can they navigate this complex procedure and safe credit score cards that can help in their credit report reconstructing journey?

Comprehending Charge Card Qualification Standard

One vital variable in credit rating card qualification post-bankruptcy is the person's credit history score. A higher credit report score signals liable economic actions and may lead to better credit card alternatives.

Additionally, people need to recognize the different kinds of credit rating cards offered. Guaranteed credit cards, for circumstances, need a cash money down payment as security, making them a lot more available for individuals with a background of insolvency. By understanding these qualification requirements, people can browse the post-bankruptcy credit history landscape better and function in the direction of rebuilding their economic standing.

Reconstructing Credit Rating After Insolvency

After personal bankruptcy, individuals can begin the procedure of restoring their debt to improve their financial security. Among the initial steps in this procedure is to obtain a safe credit scores card. Protected bank card require a cash down payment as security, making them much more accessible to people with a personal bankruptcy history. By utilizing a secured bank card responsibly - making timely repayments and keeping balances reduced - individuals can demonstrate their creditworthiness to potential lenders.

Another strategy to rebuild debt after personal bankruptcy is to end up being a certified customer on a person else's credit report card (secured credit card singapore). This allows individuals to piggyback off the primary cardholder's positive credit rating, possibly improving their own credit rating

Constantly making on-time payments for expenses and financial debts is vital in restoring credit rating. Repayment background is a significant consider determining credit report, so demonstrating responsible monetary actions is important. Additionally, regularly keeping an eye on credit rating records for mistakes and errors can aid make certain that the information being reported is appropriate, more aiding in the debt rebuilding process.

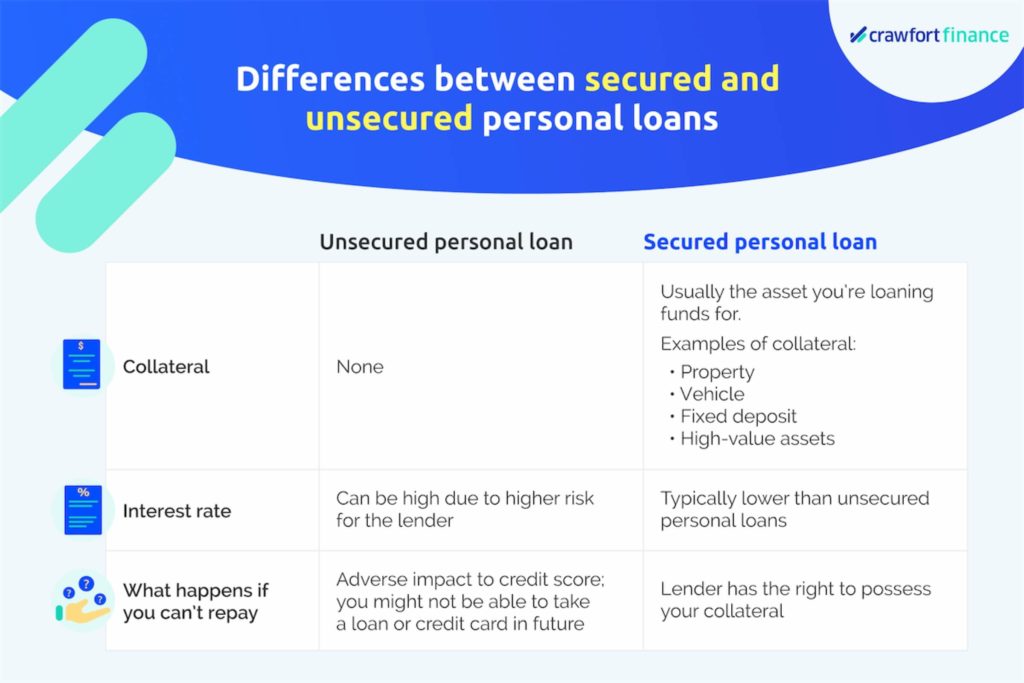

Protected Vs. Unsecured Credit Rating Cards

When considering charge card choices, people might encounter the option in between secured and unprotected bank card. Guaranteed bank card require a cash deposit as collateral, commonly equivalent to the credit history restriction given. This down payment secures the company in case the cardholder defaults on repayments. Safe cards are frequently suggested for people with inadequate or no credit report, as they supply a method to construct or reconstruct credit rating. On the various other hand, unsecured bank card do not need a down payment and are approved based upon the cardholder's credit reliability. These cards are more typical and normally come with greater credit score limits and reduced costs contrasted to secured cards. Nevertheless, people with a background of personal bankruptcy or bad credit might find it testing to receive unprotected cards. Choosing in between secured and unsecured bank card depends upon a person's monetary circumstance and debt goals. While protected cards offer a course to enhancing credit scores, unsafe cards offer more adaptability but might be more difficult to obtain for those with a struggling credit rating.

Applying for Credit Report Cards Post-Bankruptcy

Having learn the facts here now talked about the differences in between protected and unprotected charge card, individuals who have gone through personal bankruptcy might currently take into consideration the process of using for credit history cards post-bankruptcy. Rebuilding credit report after insolvency can be difficult, yet acquiring a charge card is a vital action towards boosting one's credit reliability. When looking for credit scores cards post-bankruptcy, it is vital to be critical and discerning in choosing the ideal options.

Furthermore, some individuals might get approved for particular unprotected charge card especially made for those with a background of personal bankruptcy. These cards might have greater charges or rate of interest, but they can still give a possibility to rebuild credit history when used sensibly. Before obtaining any charge card post-bankruptcy, it is a good idea to examine the terms and conditions thoroughly to recognize the fees, interest rates, and credit-building possibility.

Credit-Boosting Techniques for Bankrupts

Reconstructing creditworthiness post-bankruptcy demands implementing effective credit-boosting techniques. For people wanting to improve their credit report after personal bankruptcy, one essential strategy is to acquire a protected bank card. Secured cards need a cash down payment that works as collateral, enabling individuals to show accountable credit report usage and repayment habits. By making timely settlements and maintaining credit report application low, these individuals can progressively restore their credit reliability.

An additional technique entails coming to be an accredited customer on someone else's debt card account. This permits individuals to piggyback off the key account owner's favorable credit report, possibly increasing their very own credit history. Nonetheless, it is important to ensure that the key account owner preserves good credit rating habits to make the most of the benefits of this technique.

In addition, consistently checking credit report reports for errors and challenging any type of mistakes can also help in boosting credit history. By remaining proactive and disciplined in their debt monitoring, individuals can slowly enhance their creditworthiness even after experiencing insolvency.

Final Thought

To conclude, discharged bankrupts can obtain debt cards by fulfilling qualification standards, restoring credit rating, recognizing the difference between secured and unsecured cards, and applying strategically. By following credit-boosting methods, such as keeping and making timely settlements credit scores usage low, bankrupt people can progressively boost their creditworthiness and accessibility to charge card. It is crucial for released bankrupts to be conscious and thorough in their monetary behaviors to efficiently browse the process of obtaining credit scores cards after go now bankruptcy.

Recognizing the rigid credit history card eligibility standards is vital for individuals looking for to obtain credit cards after personal bankruptcy. While secured cards use a path to boosting credit report, unsecured cards give more adaptability but might be more difficult to obtain for those with a distressed credit score history.

In final thought, released bankrupts can acquire credit report cards by satisfying eligibility standards, reconstructing credit scores, recognizing the difference in between protected and unprotected cards, Learn More and applying purposefully.

Report this page